Accounting plays a crucial role in every business, but not all accounting serves the same purpose. Two of the most important branches are Tax Accounting and Financial Accounting. While both deal with financial data, their objectives, rules, and reporting methods differ significantly. In this blog, we'll explain the difference between tax accounting and financial accounting in simple terms.

What Is Financial Accounting?

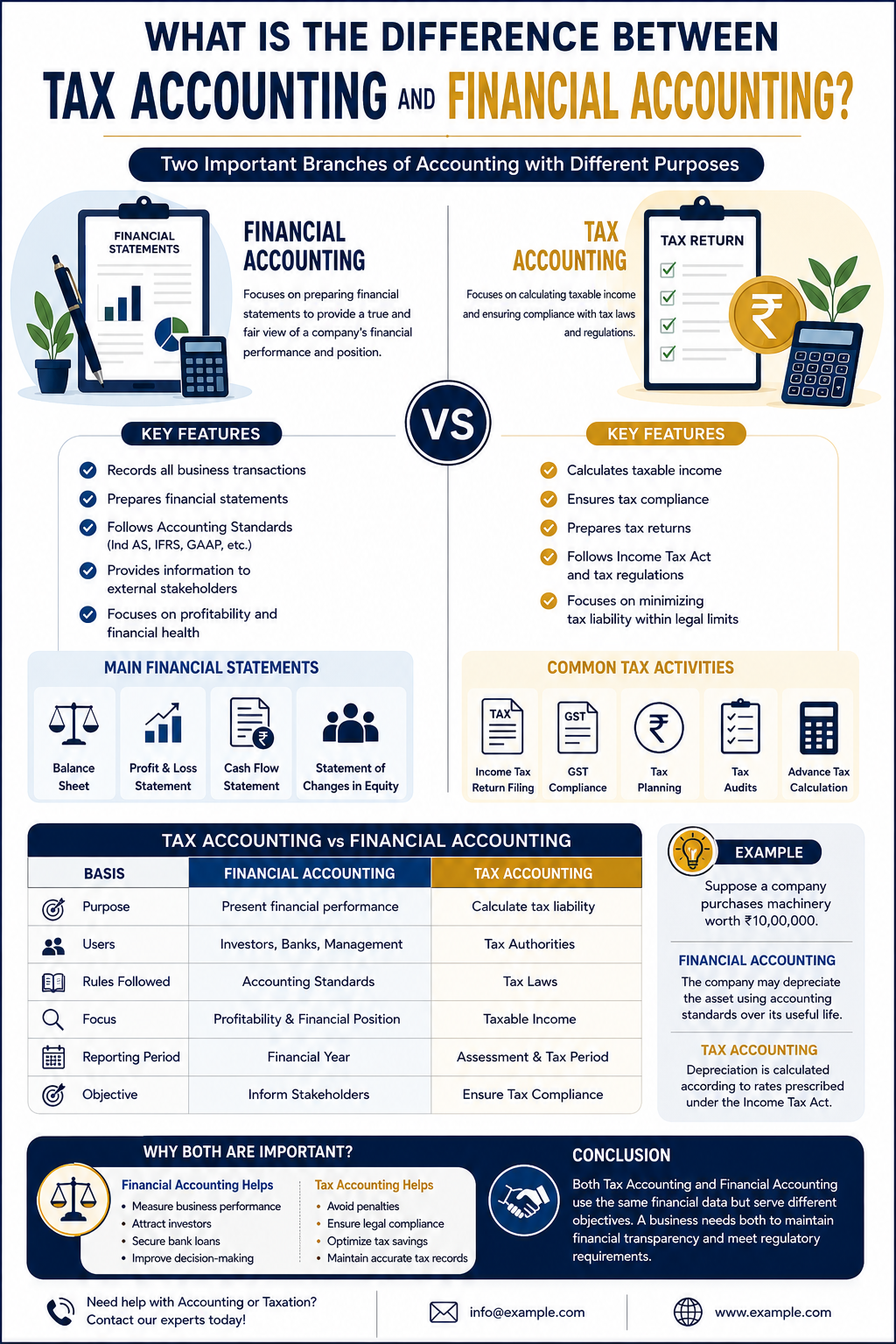

Financial accounting focuses on preparing financial statements that provide a clear picture of a company's financial performance and position.

The primary goal is to help stakeholders such as investors, lenders, management, and regulators make informed decisions.

Key Features of Financial Accounting

- Records all business transactions

- Prepares financial statements

- Follows accounting standards (Ind AS, IFRS, GAAP, etc.)

- Provides information to external stakeholders

- Focuses on profitability and financial health

Main Financial Statements

- Balance Sheet

- Profit & Loss Statement

- Cash Flow Statement

- Statement of Changes in Equity

What Is Tax Accounting?

Tax accounting focuses on calculating taxable income and ensuring compliance with tax laws and regulations.

Its primary objective is to determine the correct tax liability and ensure timely filing of tax returns.

Key Features of Tax Accounting

- Calculates taxable income

- Ensures tax compliance

- Prepares tax returns

- Follows Income Tax Act and tax regulations

- Focuses on minimizing tax liability within legal limits

Common Tax Activities

- Income Tax Return (ITR) Filing

- GST Compliance

- Tax Planning

- Tax Audits

- Advance Tax Calculation

Tax Accounting vs Financial Accounting

| Basis | Financial Accounting | Tax Accounting |

|---|---|---|

| Purpose | Present financial performance | Calculate tax liability |

| Users | Investors, Banks, Management | Tax Authorities |

| Rules Followed | Accounting Standards | Tax Laws |

| Focus | Profitability & Financial Position | Taxable Income |

| Reporting Period | Financial Year | Assessment & Tax Period |

| Objective | Inform Stakeholders | Ensure Tax Compliance |

Example of the Difference

Suppose a company purchases machinery worth ₹10,00,000.

Financial Accounting

The company may depreciate the asset using accounting standards over its useful life.

Tax Accounting

Depreciation is calculated according to rates prescribed under the Income Tax Act.

As a result, the depreciation amount may differ in both records, creating a difference between accounting profit and taxable profit.

Why Are Both Important?

A business needs both financial accounting and tax accounting because they serve different purposes.

Financial Accounting Helps

- Measure business performance

- Attract investors

- Secure bank loans

- Improve decision-making

Tax Accounting Helps

- Avoid penalties

- Ensure legal compliance

- Optimize tax savings

- Maintain accurate tax records

Which Is More Important?

Neither is more important than the other.

Financial accounting helps businesses understand how they are performing, while tax accounting ensures compliance with tax laws and proper tax management.

Successful businesses use both to maintain financial transparency and meet regulatory requirements.

Conclusion

Financial accounting and tax accounting may use the same financial data, but they have different objectives. Financial accounting focuses on presenting a company's financial position to stakeholders, while tax accounting focuses on calculating taxes and complying with tax regulations.

Understanding the difference between the two helps businesses maintain accurate records, improve financial management, and stay compliant with tax laws.

Need help with accounting, taxation, GST, or financial reporting? Contact our experts for professional assistance.