Every business owner wants to reduce taxes legally while maximizing profits. One of the most effective ways to achieve this is by claiming eligible business expenses. Understanding which expenses qualify for tax deductions can significantly lower your taxable income and help you save money. In this guide, we'll explain how business expenses reduce tax liability, what expenses are deductible, and the best practices for maintaining proper financial records.

What Are Business Expenses?

Business expenses are the costs incurred while operating your business. These expenses are generally deductible if they are ordinary (common in your industry) and necessary (help your business operate or generate income).

The more legitimate business expenses you claim, the lower your taxable profit becomes, which ultimately reduces your income tax liability.

How Business Expenses Reduce Tax Liability

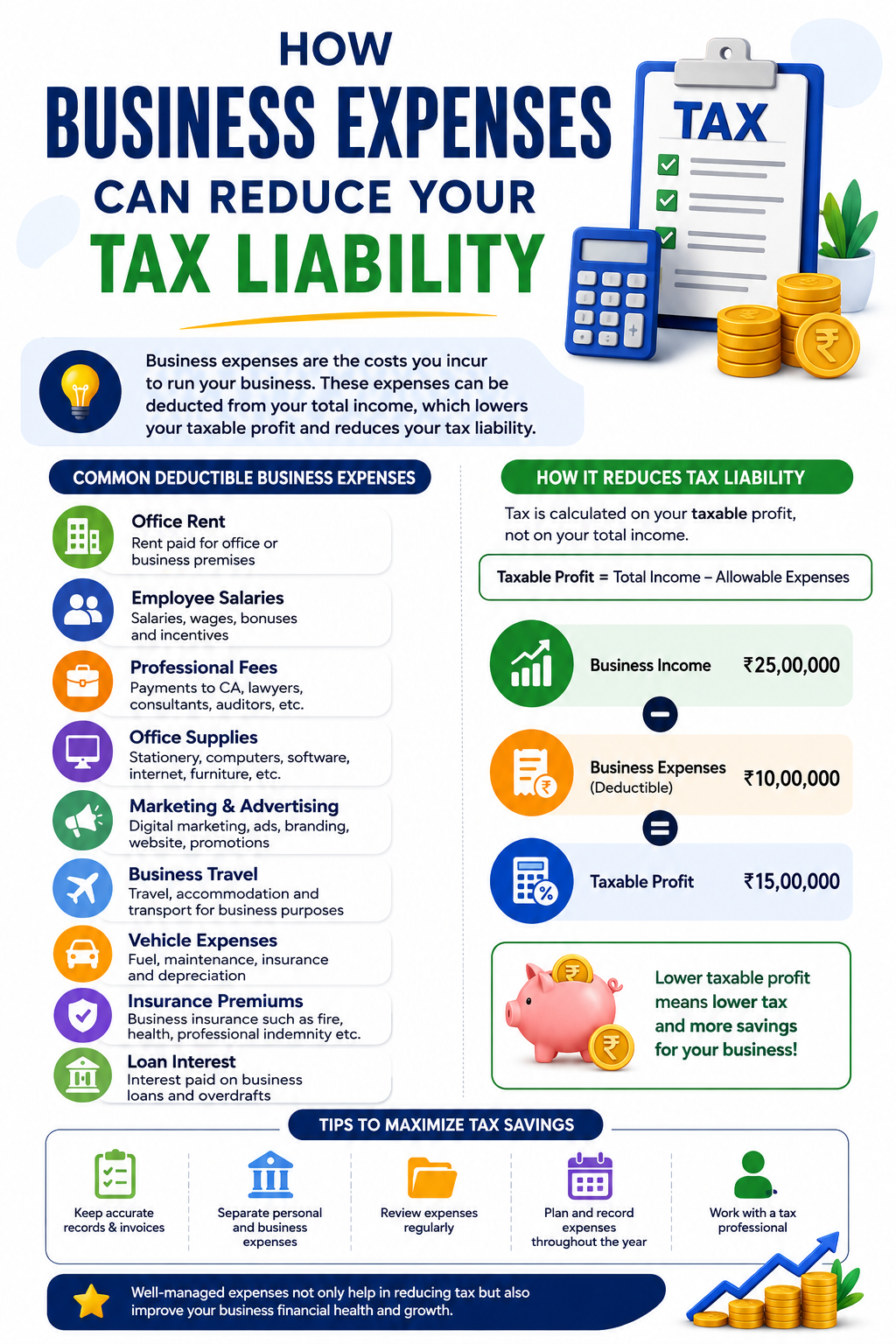

Your tax is calculated on your taxable profit—not your total revenue.

Formula:

Taxable Profit = Total Business Income − Allowable Business Expenses

For example:

- Business Revenue: ₹25,00,000

- Business Expenses: ₹10,00,000

- Taxable Profit: ₹15,00,000

Since tax is calculated on ₹15,00,000 instead of ₹25,00,000, your overall tax burden is reduced.

Common Business Expenses That Are Tax Deductible

1. Office Rent

Rent paid for office space, warehouses, or commercial premises is generally deductible.

2. Employee Salaries

Monthly salaries, bonuses, incentives, and employer contributions paid to employees can qualify as business expenses.

3. Professional Fees

Payments made to Chartered Accountants, lawyers, consultants, auditors, or tax professionals are deductible.

4. Office Supplies

Expenses for stationery, printing, computers, furniture, internet, and software subscriptions can often be claimed.

5. Utility Bills

Electricity, water, telephone, internet, and other business utility expenses are generally deductible.

6. Marketing and Advertising

Costs for digital marketing, SEO, Google Ads, social media advertising, website development, branding, and promotional materials may qualify.

7. Business Travel

Travel undertaken for business meetings, client visits, conferences, accommodation, and transportation can be deductible when properly documented.

8. Vehicle Expenses

Fuel, maintenance, insurance, and depreciation relating to vehicles used for business purposes may be claimable, subject to applicable tax rules.

9. Loan Interest

Interest paid on business loans is generally deductible, while repayment of the loan principal is typically not.

10. Insurance Premiums

Business insurance such as professional indemnity, fire insurance, and commercial property insurance may qualify as deductible expenses.

Expenses That May Not Be Deductible

Certain personal or non-business expenses generally cannot be claimed, such as:

- Personal shopping

- Family vacations

- Personal vehicle expenses unrelated to business

- Personal household expenses

- Personal entertainment expenses

Keeping business and personal expenses separate helps avoid compliance issues.

Importance of Maintaining Proper Records

Claiming deductions is easier when your financial records are organized.

Maintain:

- Purchase invoices

- GST invoices

- Bank statements

- Expense receipts

- Salary records

- Loan documents

- Rent agreements

- Utility bills

Well-maintained records also simplify audits and tax return preparation.

Tips to Maximize Tax Savings Legally

- Record expenses throughout the year instead of waiting until tax season.

- Use dedicated business bank accounts.

- Maintain digital copies of invoices and receipts.

- Reconcile your accounts every month.

- Review expenses regularly to identify deductible costs.

- Work with a qualified tax professional to ensure compliance with current tax laws.

Common Mistakes to Avoid

- Mixing personal and business expenses.

- Claiming unsupported expenses.

- Losing receipts and invoices.

- Ignoring small recurring expenses.

- Delaying bookkeeping until year-end.

These mistakes can increase taxable income or lead to unnecessary disputes during assessments.

Final Thoughts

Reducing your tax liability doesn't always require complex tax strategies. Often, the biggest savings come from accurately recording and claiming legitimate business expenses. Good bookkeeping, proper documentation, and timely financial reviews can help you minimize taxes while staying fully compliant.

Whether you're a startup, freelancer, partnership firm, or private limited company, understanding deductible business expenses is an essential part of smart financial management.